(Direct Data Access via Snowflake Also Available)

Article

Loans & MSRs: Managing model assumptions and tuners the easy way

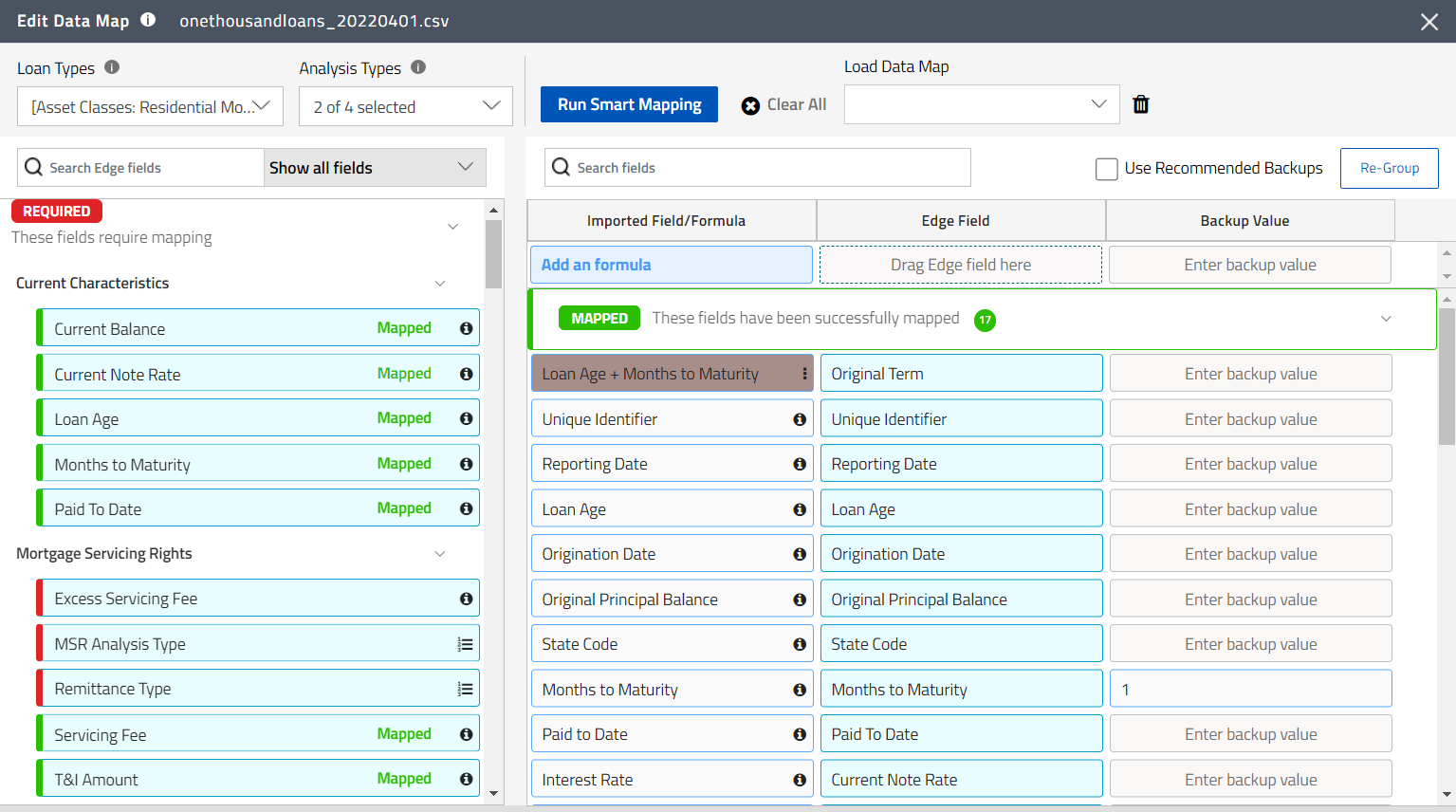

One of the things that makes modeling loan and MSR cash flows hard is appropriately applying assumptions to individual loans. Creating appropriate assumptions for each loan or MSR segment is

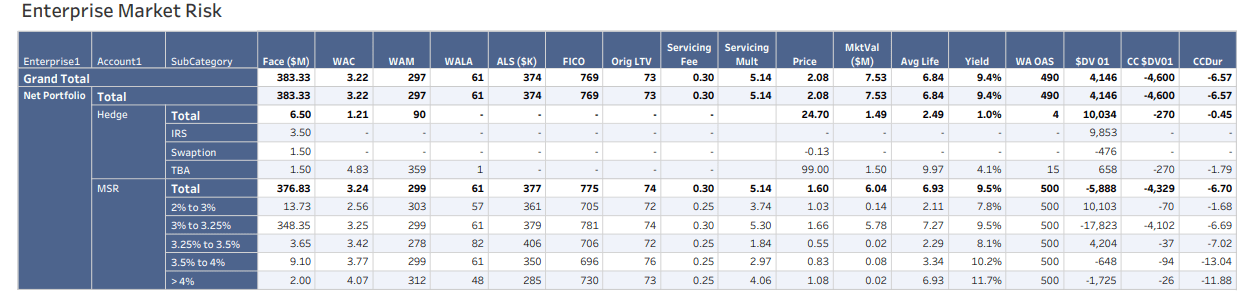

How an MSR Analytical Solution Can Boost Your Mortgage Banking Business

And why it's probably less expensive than you think Mortgage servicing rights (MSRs) are complex and volatile assets that require careful management and analysis. Inherent in MSR risk management is

What Do 2024 Origination Trends Mean for MSRs?

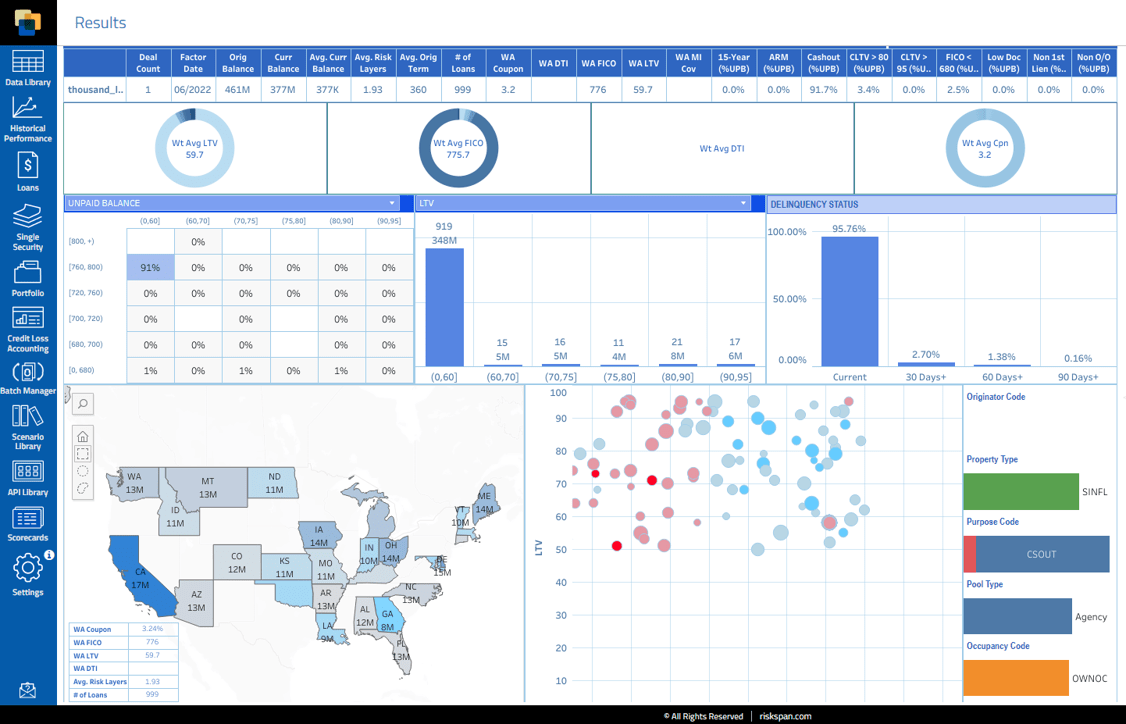

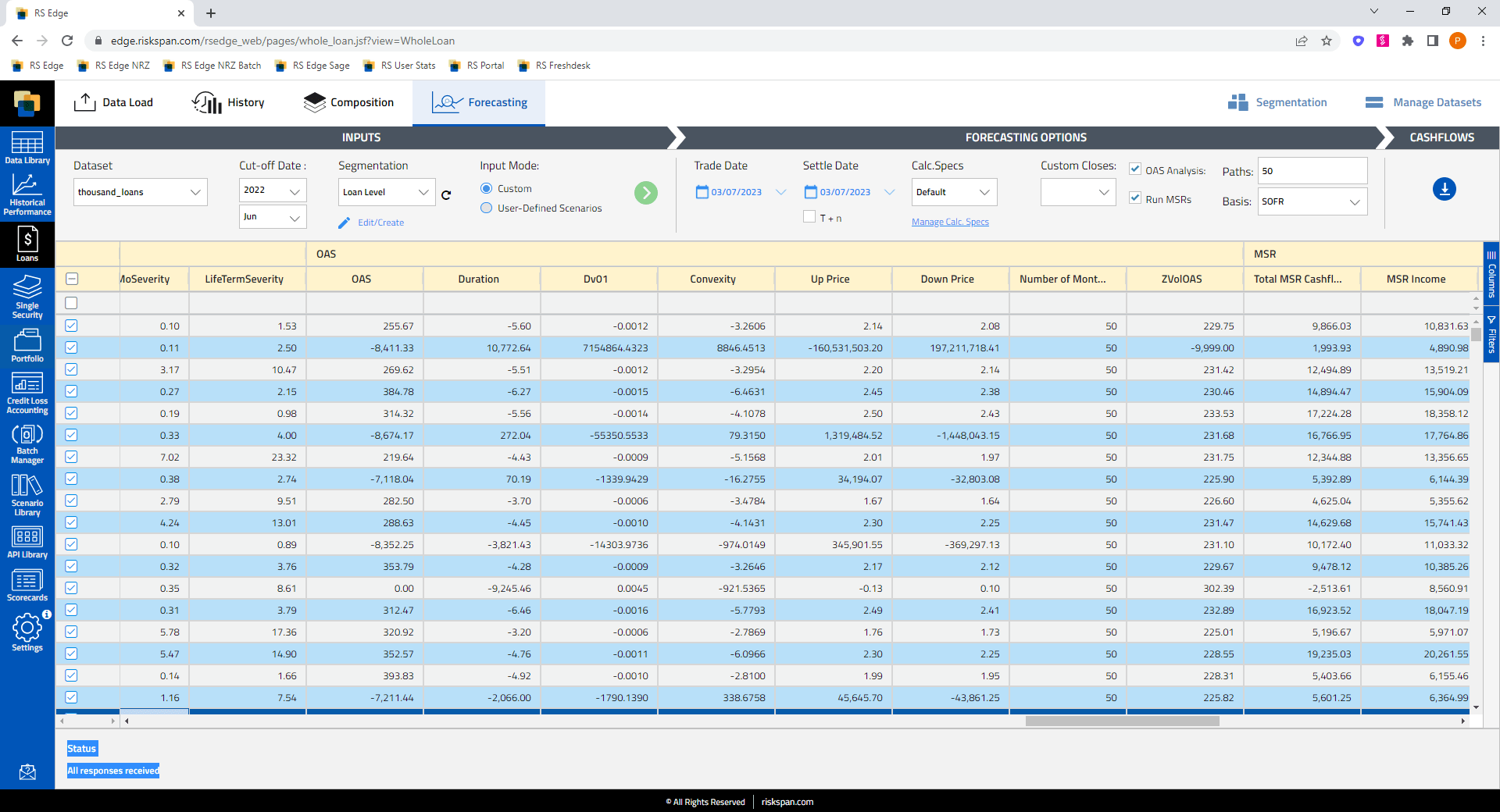

While mortgage rates remain stubbornly high by recent historical standards, accurately forecasting MSR performance and valuations requires a thoughtful evaluation of loan characteristics that go beyond the standard "refi incentive"

GenAI Applications for Loans and Mapping Data

RiskSpan is actively furthering the advancement of several GenAI applications aimed at transforming how mortgage loan and private credit investors work and maximizing their efficiency and performance. They include: 1.

Celebrating Women’s Contributions by the Numbers

Because we're a data company after all. RiskSpan commemorates International Women's Day by taking note of the remarkable people behind these numbers.

![Enriching Pre-Issue Intex CDI Files with [Actual, Good] Loan-Level Data](https://riskspan.com/wp-content/uploads/2024/03/Picture1-1024x576.png)

Enriching Pre-Issue Intex CDI Files with [Actual, Good] Loan-Level Data

The way RMBS dealers communicate loan-level details to prospective investors today leaves a lot to be desired. Any investor who has ever had to work with pre-issue Intex CDI files

RiskSpan to Launch Usage-based Pricing for its Edge Platform at SFVegas 202...

New innovative pricing model offers lower costs, transparency, and flexibility for analytics users RiskSpan, a top provider of cloud-based analytics solutions for loans, MSRs, structured products and private credit, announced

What is the Draw of Whole Loan Investing?

Mortgage whole loans are having something of a moment as an asset class, particularly among insurance companies and other nonbank institutional investors. With insurance companies increasing their holdings of whole

RiskSpan, Dominium Advisors Announce Market Color Dashboard for Mortgage Lo...

Register for FREE Access ARLINGTON, Va., January 24, 2024 – RiskSpan, the leading tech provider of data management and analytics services for loans and structured products, has partnered with tech-enabled

The future of analytics pricing is RiskSpan’s Usage-based delivery model

Usage-based pricing model brings big benefits to clients of RiskSpan's Edge Platform Analytic solutions for loans, MSRs and structured products are typically offered as software-as-a-service (SaaS) or “on-prem” products, where

RiskSpan’s Top 3 GenAI Applications for 2024

In the dynamic landscape of fixed-income securities, the role of generative artificial intelligence (GenAI) has become increasingly prominent. This transformative force is shaping the future of data, analytics, and predictive

Connect with us at SFVegas 2024

RiskSpan is delighted to be sponsoring SFVegas 2024! Connect with our team there to learn how we can help you move off your legacy systems, streamline workflows and transform your