(Direct Data Access via Snowflake Also Available)

Article

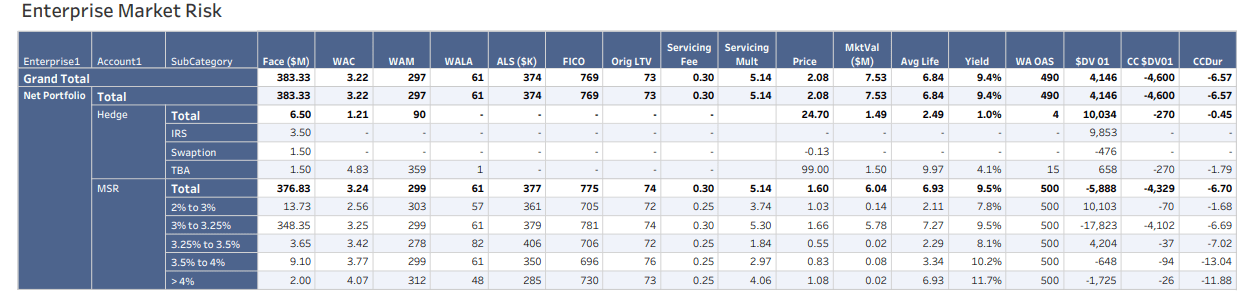

Navigating Headwinds with Data and AI: July Models & Markets Recap

Register here for next month’s call: Thursday, August 21st, 2025, 1 p.m. Each month, we host a Models & Markets call to offer our insights into recent model performance, emerging

Humans in the Loop: Ensuring Trustworthy AI in Private ABF Deal Modeling

As generative AI becomes a powerful tool in Private asset-backed finance (ABF), the need for precision and transparency is more critical than ever. At RiskSpan, we’re applying Large Language Models

June 2025 Models & Markets Update – Predictive Power Amid Economic Uncertai...

Register here for next month’s call: Thursday, July 17th, 2025, 1 p.m. Each month, we host a Models & Markets call to offer our insights into recent model performance, emerging

Private Credit Market Pulse: What LPs Want from Their Data and How to Deliv...

Limited Partners (LPs) continue to demand better data, faster, and with full transparency. At this week’s Private Credit Tech Summit in New York, I moderated a panel of industry leaders

RiskSpan’s August 2025 Models & Markets Call

Register here for our next monthly model update call: Thursday, August 21st at 1:00 ET. For highlights from our most recent call (July), click here. Contact us to learn more

Design Smarter — How AI is Changing UX from Idea to Execution

AI is revolutionizing everything, and the UX design process is no exception. From the earliest conceptual ideas all the way through to final execution, the transformation is not just about

Models & Markets Update – May 2025

Register here for next month's call: Friday, June 20th, 2025 (pushed back one day on account of Juneteenth). Each month, we host a Models & Markets call to offer our

Using LLMs as judges for validating deal cash flow models: A new frontier i...

As securitization models become increasingly complex and differentiated, validation becomes a critical challenge. We’ve experimented with an innovative approach that leverages large language models (LLMs) as impartial judges to validate

Mounting Pressure in Non-QM Credit: What March 2025 Data Signals for Risk M...

This is a monthly update on non-QM delinquency rate and roll rate trends based on the March 2025 remittance data. Similar to last month's post, I use the CoreLogic Non-Agency

RiskSpan’s April 2025 Models & Market Call: Credit Model v7, Prepay Volatil...

Register here for our next monthly model update call: Thursday, May 15th at 1:00 ET. Note: This post contains highlights from our April 2025 monthly modeling call, which delivered insights

RiskSpan Announces the Appointment of Howard Kaplan and Susan Mills to Advi...

Arlington, VA – April 10, 2025 – RiskSpan, a leading provider of innovative analytics and risk management and data analytics for loans, securities and private credit,is pleased to announce the

From AI Hype to Helpful Assistant: AI Agents are coming soon to the RiskSpa...

When agentic AI first hit the scene, we were intrigued—but skeptical. Was this just another over-hyped trend or something that could drive real value? Fast forward a few months, and